Indian Retail Industry 2012 - 2013

Rajesh Thambala – Research Analyst

1. Introduction

T

|

2. Retail Industry in India

The total concept and idea of shopping has undergone a vast drawing change in terms of format and consumer buying behavior, ushering in a revolution in shopping in India. Modern retailing has entered into India as is observed in the form of sprawling shopping centers, multi-storied malls and the huge complexes that offer shopping, entertainment and food all under one roof.

The Indian retail industry has experienced growth of 10.6% between 2010 and 2012 and is expected to increase to USD 750-850 billion by 2015. The industry has long way to go as there is a huge opportunity in streamlining the sector. Indian retail sector is gradually inching its way towards becoming the next boom industry.

Food and Grocery is the largest category within the retail sector with 60 % followed by Apparel and Mobile segment.

3. Organized & Unorganized Retail sector in India

Currently India constitutes only 8% of organized retail and remaining 92% is left unorganized, which may grow much faster than traditional retail. It is expected to gain a higher share in the growing pie of the retail market in India. Various estimates put the share of organized retail as 20% by 2020.

The growth pattern in organized retailing and in the consumption made by the Indian population may follow a rising graph helping the newer businessmen to enter the India Retail Industry.

The country's traditional retail industry is expected to grow at an average annual rate of 5% over the next year, while the organised retail is estimated to register a growth rate of around 25% during this period.

|

5. Foreign Direct Investment (FDI) in Indian retail

The current sign of reforms by the Government to initiate Foreign Direct Investment (FDI) in various sectors is bringing a new enthusiasm to the investment climate in India.

The recent announcement by the Indian government with Foreign Direct Investment (FDI) in retail, especially allowing 100% FDI in single brands and multi-brand FDI has created positive sentiments in the retail sector.

6. Foreign foot print in Indian Retail market

In India the vast middle class and its almost untapped retail industry are the key attractive forces for global retail giants wanting to enter into newer markets

Foreign entrants in the Indian segment are as follows:

- Germany-based Metro Cash & Carry opened six wholesale centres in the country.

- Walmart with Bharti Retail, owner of Easyday stores.

- British retailer Tesco Plc (TESCO) signed an agreement with Trent Ltd (Trent), the retail arm of Tata Group to set up cash-and-carry stores.

- Carrefour opened its first cash-and carry store in New Delhi.

7. Key drivers of retail growth in India

The growing disposable income in the country is resulting in increasing consumer spending habits. A large young working population with median age of 24 years, nuclear families in urban areas, along with increasing workingwomen population and emerging opportunities in the services sector are going to be the key factors in the growth of the organized Retail sector in India.

Factors driving the organised retail sector include the following:

- Higher incomes driving the purchase of essential and nonessential products

- Evolving consumption patterns of Indian customers

- New technology and lifestyle trends creating replacement demand

- Increase in rural income as well as urbanization

- Increase in easy access to credit and consumer awareness

- Growth of modern trade format across urban, Tier I, Tier II and Tier III cities and towns

- Rapid urbanization and growing trend towards nuclear families

- FDI in specialty stores: Multi-brand organized retail in specialty stores such as Consumer Electronics, Footwear, Furniture and Furnishing etc. are expected to expand and mature in the next few years. However the policy condition on sourcing will continue to be a major bottleneck for FDI in many of these segments

- Dominance of unorganized retail: Flexible credit options and convenient shopping locations may help traditional retail to continue its dominance in retail sector.

- Growth in small cities and towns: Stiff competition and saturation of urban markets is expected to drive domestic retail players to tap the potential in small cities

9. Indian Retail Strategy

As a strategy, retailers continue to focus on improving the operations machinery of the business, shifting to low cost channels, promoting private labels, emphasis on increasing customer base, improving in cost structure, discounts and offers and innovative strategies such as ‘flat discounts’, sale during wee hours of morning or late till midnight, are some of them.

10. Retail Opportunity

According to 2012 Global Retail Development Index India has secured 5th rank in market attractiveness.

India remains a high-potential market with accelerated retail growth of 15 to 20 percent expected over the next five years. Growth is supported by strong macroeconomic conditions, including a 6 to 7 percent rise in GDP, higher disposable incomes, and rapid urbanization. Yet, while the overall retail market contributes to 14 percent of India's GDP, organized retail penetration remains low, at 5 to 6 percent, indicating room for growth.

India’s large and aspiring middle class of 75 million households or 300 million individuals want products that are value-driven. The country’s 500 million people under the age of 25 have access to more money that has additionally resulted in independence, aspirations and a demand for products.

“India's changing FDI climate provides an interesting dynamic to several international retailers' entry and expansion plans”

Companies such as Gap, IKEA, and Abercrombie & Fitch are stepping up inquiries to enter the market, while others are seeking local partners. Hypermarkets and supermarkets continue to dominate, but cash-and-carry is growing fast, with significant expansion from Bharti Wal-Mart, Metro Group, Carrefour etc.

11. Technology in Indian Retail

In India, the use of IT is confined to the organised sector, a small proportion of the retail industry. In general, mid-sized players are only using point-of-sale (POS) and basic systems like stores software, SKU software, etc. However, small modern retailers have hardly made investments in IT infrastructure.

Barcode scanning was the first major technology application adopted by Indian retailers that ushered in a new level of automation to front-end point-of-sale processes. Using scanning technologies made cashiers more productive, reduced the number of errors at the register and made the inventory and buying trends more visible and accurate.

India’s retail sector has undergone several technology evolutions to enable retailers to increase efficiency, improve customer service and become more competitive. India’s retail sector, today, is advanced in its adoption of basic IT systems and infrastructure like ERP, networks etc. Medium and large retailers are in the process of establishing robust transaction systems including suitable POS systems, merchandise management systems, CRM systems, and radio-frequency identification

Need for IT solutions - Indian retail

Most Indian retailers need to use advanced IT products and solutions like replenishment planning, world-class supply chain and logistics management systems, business intelligence and analytics systems, warehouse management systems, etc. The growth of the Indian economy is bringing about several changes in consumer demand and purchase patterns. The Indian retail market is difficult to predict, consumers are evolving, and retailers are expanding operations, further driving the need for IT adoption.

12. Online Retail in India

Market is small now, but will grow rapidly in coming years

India’s eCommerce market is at an early stage but is expected to see huge growth over the next four to five years. Over the past 12 months, venture capitalists have invested heavily in India’s eCommerce market, new players have emerged, and the eCommerce ecosystem has developed, presenting a huge opportunity for companies willing to work through some of the logistics and payments challenges in India.

An increasing number of global companies are eyeing the rapidly growing eCommerce market in India. As the world’s 11th-largest economy (and fourth-largest emerging economy after BRIC peers China, Brazil, and Russia), India is starting to appear on eBusiness organizations’ lists of key international markets.

| |

India will grow quickly off a small base. India’s eCommerce market is poised to grow by more than five-fold by 2016 as the number of online buyers and per capita online spending increase rapidly. This market is gaining more attention as global brands look to markets that are in the early stages of eCommerce adoption but offer significant long-term potential.

Almost 75% of India’s internet users are under the age of 34. As many of them move into the earning segment in the years to come, Internet commerce is expected to get a significant boost.

The world's consumers spend on average 22 percent of their disposable income on purchases on the Internet, with Indians at the forefront (33 per cent). Chinese and Indians spend the most time shopping online at 8 hours per month, while French, Finnish, Japanese and Spanish allocate less than four hours to the activity.

| |

13. Online retail vendors performance in Indian in 2012

Online Retail sites recorded 37.5 million visitors in July 2012, up from 26.1 million in July 2011. Gavane stated that Snapdeal and Flipkart recorded 7.5 million visitors, while Myntra and Jabong have around 5 million visitors as indicated in the graph below.

Apparel is the fastest online retail category in the country, recording a 362% YoY growth and total audiences reach of 13.4%, followed by Consumer goods which recorded 119% YoY growth and has 2.9% audience reach, and sports/outdoor goods which recorded 100% YoY growth and has 2.8% audience reach.

Flipkart has an average transaction size of $35 (Rs 1945.6), Yebhi has an average transaction size of $27 (Rs 1501) and Myntra has an average transaction size of $24 (Rs 1334). Myntra had stated an average transaction size of Rs 1250 in June 2012.

14. Kids apparel

Indian kids-wear market is growing at a compounded annual growth rate of about 20 per cent and is likely to reach Rs 80,000 crore by 2015. The report has concluded that kids fashion has percolated down to tier-II and tier-III cities like Dehradun, Chandigarh, Pune, Nasik, Indore, and Varanasi so on.

AllSchoolStuff.com, FirstCry, M2C and Babyoye.com are some of the sites that are logging on to the online opportunity. Some of the online kid’s retail business added 10% of their total revenues from this segment last year.

Indian online retail vendors agree that this is a disorganized market and they have huge opportunity to expand their wings and grab the market.

Targeting this group early on clearly seems to be on the agenda of most of the Indian ecommerce players.

- Key Numbers

- There are currently over 10 websites that only sell products meant for children

- Kids' retail market stands at Rs 22,000 crore, as estimated by Technopak

- In three years, the overall kids¡¦ retail market will be worth Rs 80,000 crore

- The kids' e-tailing market is expected to swell to Rs 1,500 crore in five year

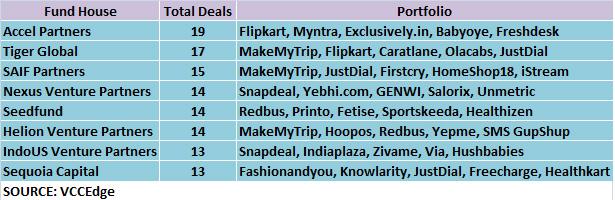

- 15. VC Investments in Indian E-commerce

52 E-Commerce companies raised close to $700 Mn in Venture Capital over the past 3 years Series A Series B Further Rounds $185 Mn across 52 firms $210 Mn across 16 firms $300 Mn across 7 firms

10 Horizontal portals (multi category retailers) have garnered over $355 Mn (half the amount Horizontal invested in the sector) $355 Mn $691 Million

§ $220 Mn of investment into 21 Apparel and Apparel & Accessories e-tailers Accessories

§ $30 million across 5 firms in the Baby Products $180 Mn category Private Label Apparel

§ Daily deals portals raised $25 Mn; however, Apparel $40 Mn Others most of them pivoted into horizontal e- 221 Mn 52 commerce $115 Mn Companies

§ 13 other niche category e-tailers raised about $61 Mn excluding Seed and Angel funding Including Flipkart’s $150 Mn round 2 Includes Home Décor, Health & Beauty, Jewelry & Groceries

16. Products that Indian online retails sell the most

The following factors are influencing this growth

- Venture capitalists are bullish on eCommerce growth

- Online grocery shopping is starting to appeal to the upper- and middle-class consumer.

- Expanding eCommerce into nonmetropolitan India

- Large retailers are looking to build an online presence

- Social media and mobile are helping accelerate eCommerce adoption

18. Conclusion

Modern retail in India could be worth US$ 175-200 billion by 2016. The Food Retail Industry in India dominates the shopping basket. The Mobile phone Retail Industry in India is already a US$ 16.7 billion business, growing at over 20 per cent per year. The future of the India Retail Industry looks promising with the growing of the market, with the government policies becoming more favorable and the emerging technologies facilitating operations.

Young Indians are driving purchases in mobile phones, fashion, accessories, food and beverages, quick service restaurants, etc. Young Indians have access to more money than before and with this have come independence, aspirations and a demand for products

The Indian retail sector is evolving rapidly and those who enter the market now can learn about local dynamics, develop market insights and establish leadership positions.

Don’t let India’s low internet penetration distract from the fact that over 50 million Indians already shop online. And this is just the beginning for this emerging marketplace. E-commerce space in India is to quickly match the growth of its overall consumer marketplace.

“The future is promising; the market is growing, government policies are becoming more favorable and emerging technologies are facilitating operations”

Indian Retail Industry 2012 - 2013

ReplyDeleteHello everyone on here my name is Fumo Sadiku living in Malindi City Kenyan I want to tell a little more about a good hearten man called Benjamin Breil Lee working with Le_meridian funding service as loan officer, Mr Benjamin Breil Lee helped me get a loan of 37,115,225.00 Shillings on my trying time trying to get back on my feet to raise my business I know there are some of you here who are in financial difficulties to talk to Mr Benjamin on what's app 1-989-394-3740 Or email his company E-Mail lfdsloans@lemeridianfds.com also with his personal E-mail on lfdsloans@outlook.com I'm so glad for what he did for me and for his Bank accountant as well Accountant Hernandez Lucas Thank you very much for your work well done.

ReplyDeleteYou certainly did it well! First off, I want to recognize your work, this was really nice! I like the style of your writings! When you have time, I want to share with you this retail market if ever you need to buy something. Retail Business in India

ReplyDeleteGood information. Keep it up.

ReplyDeleteSun Pharmaceuticals Ltd

Dabur India Ltd

Exide Industries Ltd

Future Retail Ltd

It was such a good post. Visit india food and grocery. Thanks for sharing.

ReplyDeleteAll kinds of apps are available here. It's An Amazing Site.

ReplyDeletereally a nice post!

visit my side. I hope it will prove helpful for you.

Retail Man POS Crack

vstfull.com

This comment has been removed by the author.

ReplyDeleteThis is a great inspiration.You put really very helpful information

ReplyDeletemovavi video suite crack

retail man pos crack

Ultra Adware Killer crack

Pixarra TwistedBrush Pro Studio Crack

vuescan pro crack

Suffescom is the ideal technological partner if you're trying to start your retail store in a small town. Whatever Retail Business Ideas for small town you choose, meticulous planning is vital to its success. Additionally, because operating a small business is both a lifestyle and a time commitment, ensure that it is one that you can envision providing you both profit and satisfaction in the long run.

ReplyDeleteBusinesses that are upgrading to internet platforms are demonstrating the paradigm change. This is because it enables businesses to profit from their efforts, build brand equity, reach a large audience, and earn income. With so many perks, it's understandable why any business would want to launch a successful online store. This is where a platform like Shopify comes in handy.

ReplyDeleteNice blog, I really found this bit quite informative. Automation has more potential in the retail industry.

ReplyDeletevery useful article keep it up

ReplyDelete5 Best Whisky Brands In India

Top 10 baby product brands in india

top 10 refrigerator brands in india

top 10 non chinese brands of smartphones in india

Thanks for sharing. Contact Dynamic Netsoft Technologies for Retail ERP software . Dynamic Netsoft Technologies is a Microsoft gold partner with decade plus experience. We're specializes in implementation of MS D365 ERP & CRM.

ReplyDeleteDownload Software for PC & Mac

ReplyDeleteYou make it look very easy with your presentation, but I think this is important to Be something that I think I would never understand

It seems very complex and extremely broad to me. I look forward to your next post,

Malwarebytes Crack

Wirecast Pro Crack

XSplit Broadcaster Crack

VSDC Video Editor Crack

Retail Man POS Crack

AVS Video Editor Crack

I'm really impressed with your writing skills, as smart as the structure of your

ReplyDeleteLatest Software Free Download

weblog. Is this a paid topic

Diskdigger crack

do you change it yourself? However, stopping by with great quality writing, it's hard to see any good blog today.

Program4pc audio convertercrack

Diskdigger-crack

Reimage pc reapir crack

pixarra pro crack

Thanks for sharing this blog info, I have find this info very useful for my PGDM course as well which i am doing from distance learning center in retail management.

ReplyDeleteThanks for sharing informative Blog. I just stumbled upon your blog and wanted to say that I have really enjoyed reading and finding knowledge.

ReplyDeleteretail industry software solutions

I'm really impressed with your writing talents, which are as smart as the structure of your article. Thank you for providing this blog information; I've found it really beneficial. custom erp solutions

ReplyDeleteVery good information Go to for professional help on public limited company finance This blog helps us to know more about it.

ReplyDeleteYour article is Good

ReplyDeleteJewelry ERP in Kerala

Innervex® Smart Store - Jewellery App in Kerala